The Fundamentals #5 – How to use AIM to stop HMRC taking money from your family?

In the fifth of our series – The Fundamentals – about going back to the basics of investing in AIM shares for Inheritance Tax (IHT) planning purposes, we look at: How to use AIM to stop HMRC taking money from your family.

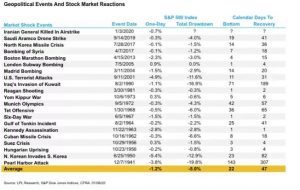

Figures released yesterday by HMRC showed they took £6.1 billion in Inheritance Tax for March – up by £0.7 billion on last year. How can clients use AIM to reduce the amount their family pays after they pass away?

One way is for a client to invest in certain AIM shares that qualify for Business Relief for 2 years and provided they are still held at death, the estate will not pay Inheritance Tax on them.

What is Business Relief?

Business Property Relief or BPR (now known as Business Relief) was first introduced in 1976 to allow family businesses to be passed down through generations free of IHT. Its scope subsequently widened and since 1996 it was made available for a range of assets, including limited companies. This means if you buy and hold shares in such companies you could potentially pass on those shares IHT free provided that:

- the shares are held for at least two years and are still held on death

- the company still qualifies for BPR at the time of the investor’s death

You could buy as few or as many shares as you wish. There is no upper limit or allowance. Provided the above conditions are met, the whole value of the investment – be it £10,000 or £10 million – should attract 100% IHT relief.

Please note, tax benefits depend on circumstances and tax rules can change.

Inheritance Tax mitigation

A Fundamental AIM Inheritance Tax portfolio achieves 100% mitigation from Inheritance Tax after only two years. Not seven years as is the case through a gifting or trust approach.

Upcoming webinar: How to use AIM for Inheritance Tax Planning? Your Questions Answered

Join Fundamental Asset Management’s Co-Founders Chris Boxall & Stephen Drabwell on Wednesday 4th May at 3pm 2022 as they answer your questions on using AIM for Inheritance Tax Planning. To register for the webinar click here.

What Would You Like To Know?

Now is the time to ask us and we will endeavour to cover it in the webinar.

Send your questions to: [email protected]

The Fundamentals Series

- Introducing The Fundamentals series

- The Fundamentals #2: How to use ISAs for Inheritance Tax (IHT) planning?

- The Fundamental #3: The perils of exit fees & support for a client’s estate

- The Fundamentals #4 – What is the Fundamental AIM Inheritance Tax Portfolio?

If you have any questions, please do not hesitate to contact our Business Development Manager Jonathan Bramall via email [email protected] or phone 01923 713 894

Our Educational Webinars also provide plenty of further information.

Fundamental Asset Management

www.fundamentalasset.com